Compliance Obligations Calculator

Project Compliance Assessment

Answer these questions to identify your key compliance obligations

Compliance Results

Why blockchain compliance isn’t a one-time task

If you think setting up a blockchain project means you’re done with legal stuff, you’re already behind. Ongoing compliance obligations in blockchain aren’t optional checklists-they’re living systems that change as laws, technologies, and regulators evolve. Unlike traditional software, blockchain is public, immutable, and often跨境 (cross-border). That means one wrong move can trigger fines, frozen assets, or even criminal charges. The European Union’s MiCA regulation, which fully kicks in on December 30, 2024, alone covers over 2,000 crypto firms operating in the EU. And it’s not just Europe. The U.S. SEC has filed over 120 enforcement actions against crypto projects since 2023. Compliance isn’t something you do once. It’s something you do every day.

What counts as an ongoing compliance obligation in blockchain?

These aren’t just vague rules. They’re specific, enforceable requirements you must track and act on. In blockchain, they fall into three buckets:

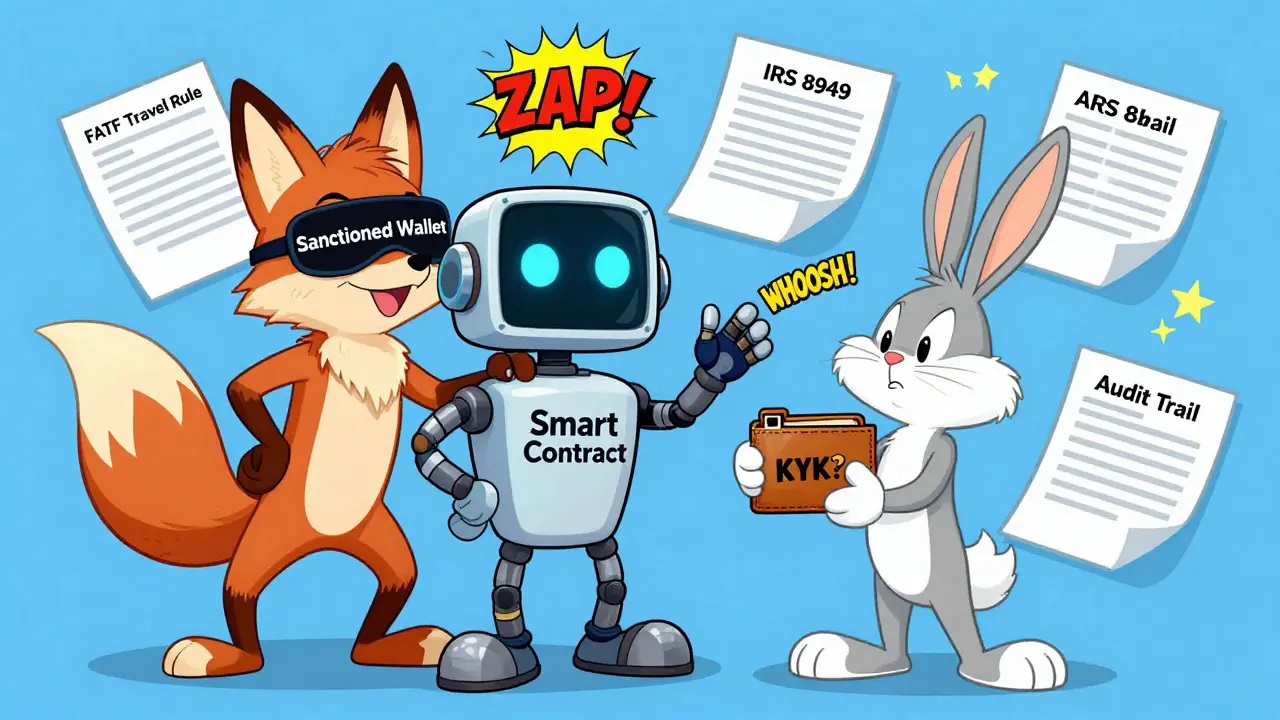

- Mandatory legal rules: Things like AML/KYC laws (e.g., FATF Travel Rule), securities regulations (SEC rules on token sales), tax reporting (IRS Form 8949 for crypto gains), and data privacy laws (GDPR for on-chain personal data).

- Contractual obligations: Agreements with exchanges, wallet providers, or auditors that require you to submit regular reports, maintain audit trails, or restrict certain token transfers.

- Voluntary standards: Industry frameworks like the Crypto Council for Innovation’s Compliance Best Practices or ISO/TC 307’s blockchain standards-these aren’t laws, but ignoring them can hurt your credibility and access to partners.

For example, if your decentralized exchange (DEX) allows users to trade tokens that the SEC considers securities, you’re legally required to verify user identities and report suspicious activity-even if your code is “decentralized.” The law doesn’t care about your tech architecture. It cares about who controls the flow of value.

How blockchain changes the game for compliance

Traditional compliance tools-paper logs, spreadsheets, annual audits-don’t work well with blockchain. Here’s why:

- Immutability: Once data is on-chain, you can’t delete it. That’s great for transparency, terrible if you accidentally store a user’s passport number or email. GDPR’s right to be forgotten clashes directly with this.

- Decentralization: If no single entity controls the protocol, who’s responsible? Regulators say “the operator.” Courts are starting to agree. In 2024, a U.S. district court ruled that the founder of a defunct DeFi lending platform was personally liable for unregistered securities sales-even though the code ran autonomously.

- Global reach: A token sold in Singapore to a user in Brazil, funded by a wallet in Germany, and tracked by a node in Japan? You’re subject to all three jurisdictions. There’s no “home base” anymore.

That’s why 73% of blockchain firms now use automated compliance tools. Manual tracking just doesn’t scale. Tools like Chainalysis, Elliptic, or ComplyAdvantage scan on-chain transactions in real time, flagging wallets linked to sanctioned entities or darknet markets. These aren’t luxuries-they’re necessities.

The cost of getting it wrong

Penalties aren’t theoretical. In 2023, a U.S.-based NFT marketplace was fined $1.2 million for failing to implement KYC on over 500,000 users. A Swiss DeFi protocol paid €850,000 after regulators found it processed transactions from Russian addresses banned under EU sanctions. And those are just the public cases.

But money isn’t the only cost. Reputation damage hits harder. In 2024, a major blockchain analytics firm lost 40% of its enterprise clients after it was revealed they had ignored a known vulnerability in their compliance reporting system. Clients didn’t leave because of the hack-they left because the company showed it didn’t take compliance seriously.

Compare that to Coinbase, which spent over $500 million on compliance between 2021 and 2024. They got fined $50 million in 2023 for AML failures-but they’re still the most trusted crypto exchange in the U.S. Why? Because they proved they’re trying. Regulators reward effort, not perfection.

How to build a real-time compliance system

You don’t need a legal team of 50. But you do need structure. Here’s what works:

- Build a living compliance register: List every law, rule, and contract that applies to you. Include: who it applies to, what you must do, when it changes, who’s responsible, and how you prove compliance. Update it every 30 days. Don’t wait for a regulator to knock.

- Automate monitoring: Use blockchain analytics platforms that alert you when a wallet on your platform matches a sanction list or shows suspicious behavior. Set thresholds-e.g., flag any transaction over $10,000 from a high-risk jurisdiction.

- Assign ownership: Don’t put compliance in a “legal department” that doesn’t understand code. Assign a compliance lead in engineering, another in operations, and one in customer support. They each know where their part of the system fails.

- Train every employee: Even your support team needs to know what a SAR (suspicious activity report) is. In 2023, a user reported a scam to a help desk agent who didn’t know to escalate it. That delay cost the company $320,000 in fines.

- Review quarterly: Set calendar reminders. Every three months, meet with your team and ask: “What new regulation came out? What did we miss? What broke?”

One DeFi startup in Wellington reduced compliance violations by 80% in 10 months using this method. They didn’t hire lawyers. They just started treating compliance like code: always testing, always updating.

What to avoid

Here are the top three mistakes blockchain teams make:

- “We’re decentralized, so we’re exempt”: Courts are rejecting this argument. If you’re marketing, fundraising, or operating the platform, you’re responsible.

- Using open-source tools without checking their compliance status: Many DeFi protocols use libraries that don’t screen for sanctions. You’re liable if your code connects to a blacklisted wallet.

- Thinking audits are enough: An annual audit is like checking your car’s oil once a year. You still need to drive safely every day.

Tools and resources you can use today

You don’t need to build everything from scratch. Here are practical tools:

- Chainalysis Reactor: Real-time blockchain monitoring for AML and sanctions screening. Used by 80% of major exchanges.

- Elliptic Fusion: Tracks on-chain risk scores and links wallets to real-world entities.

- ComplyAdvantage: AI-powered compliance platform that updates regulatory lists daily.

- ISO/TC 307: International blockchain standards body. Their guidelines are free and updated quarterly.

- FATF Guidance on Virtual Assets: The global standard for crypto AML. Download it. Read it. Follow it.

For small teams, start with one tool and one regulation. Focus on KYC for your users. Then add transaction monitoring. Then tax reporting. Don’t boil the ocean.

The future: AI, regulation, and what’s coming

By 2026, 85% of blockchain compliance will be automated. AI will predict regulatory changes before they’re published. For example, if a new EU directive is leaked, AI models trained on past laws can flag what it might mean for your tokenomics. The EU’s MiCA is just the start. The U.S. is working on a federal crypto bill that could classify tokens by function (utility, security, payment). That will force every project to reclassify their tokens-and update their compliance systems.

Blockchain itself is becoming a compliance tool. Projects like the World Bank’s blockchain-based bond issuance use smart contracts to automatically enforce compliance rules. If a user isn’t KYC’d, the contract blocks the transaction. No human needed. That’s the future: compliance baked into the code, not bolted on after.

Final thought: Compliance is your competitive edge

Most blockchain teams see compliance as a cost. The smart ones see it as a moat. If you’re the only project in your niche that can prove you’re fully compliant, you’ll attract institutional investors, bank partnerships, and enterprise clients. You’ll survive when the next crackdown hits. And you’ll be the one people trust when others fail.

Do I need to comply with blockchain regulations if I’m not in the U.S. or EU?

Yes. If your blockchain project serves users in the U.S., EU, or any jurisdiction with crypto laws, you’re subject to their rules-even if you’re based in New Zealand, Nigeria, or Singapore. Regulators enforce jurisdiction based on user location, not company headquarters. A single user from California can trigger SEC action. Always check where your users are.

Can I use smart contracts to automate compliance?

Absolutely. Smart contracts can enforce KYC checks, block transactions to sanctioned wallets, and auto-report tax data. But they’re not foolproof. You still need human oversight to update the rules when laws change. A smart contract can’t interpret a new SEC ruling-it can only follow code. Use it as a tool, not a shield.

What if I can’t afford compliance software?

Start with free tools. Use the FATF Travel Rule checklist, download the ISO/TC 307 guidelines, and build a simple Google Sheet to track your obligations. Assign one team member to check regulatory updates weekly. Many small teams save thousands by doing this manually before investing in paid tools. The key is consistency, not cost.

How often do blockchain regulations change?

Constantly. In 2024 alone, over 40 countries updated their crypto regulations. The EU’s MiCA rollout, the U.S. SEC’s enforcement actions, and Japan’s revised Financial Instruments and Exchange Act all happened within 12 months. Treat compliance like a software update: check it every 30 days. If you wait for a notice from a regulator, you’re already late.

Is blockchain truly anonymous, and does that help me avoid compliance?

No. Blockchain is pseudonymous, not anonymous. Every transaction is public. Forensic tools like Chainalysis can link wallet addresses to real identities with 80%+ accuracy. Regulators don’t need to know your name-they need to know who controls the wallet. If you’re running a platform, you’re the one who controls access. That makes you responsible.

Categories