When you hear "liquidity provider" in DeFi, you might picture someone quietly earning passive income by depositing crypto into a pool. But behind that simple idea is a high-stakes game of math, incentives, and risk-where the top 5% of users make 2.8% monthly, while 68% of participants lose money to impermanent loss, even when they earn rewards. This isn’t just about staking. It’s about understanding how protocols pay you to take on risk-and why most people don’t survive long enough to profit.

How Liquidity Providers Actually Make Money

Liquidity providers (LPs) aren’t depositors. They’re market makers. Every time someone swaps ETH for USDC on Uniswap, the price shifts slightly. That shift creates slippage-costs that add up to $12.7 billion annually across DeFi. LPs absorb that slippage. In return, they get two things: a cut of every trade fee, and often, extra tokens. On Uniswap V3, if you put $10,000 into an ETH/USDC pool, you earn roughly 0.5% to 1.2% per year just from trading fees. That sounds low-until you realize it’s automatic. No need to stake, no lockups. Just leave your funds in the right price range, and you get paid every time someone trades. But here’s the catch: if ETH drops 30% while you’re in the pool, your share of the pool might be worth 20% less than when you started. That’s impermanent loss-and it eats rewards alive. To fight this, protocols add token rewards. SushiSwap pays out MAGIC tokens. Curve gives CRV. PancakeSwap throws in CAKE. These can push annual yields to 8-15%. But those numbers are misleading. They assume your reward token doesn’t crash. In 2025, over 22 out of 30 protocols saw their incentive tokens lose 37-89% of their value. Suddenly, your 12% APY becomes a 5% loss.The Rise of Protocol-Owned Liquidity (POL)

The smartest protocols stopped renting liquidity. They started buying it. OlympusDAO pioneered Protocol-Owned Liquidity (POL). Instead of paying users with tokens, the protocol uses its treasury to buy LP positions directly. As of December 2025, 99.8% of OHM/DAI liquidity was owned by Olympus itself. That means no more users quitting when rewards drop. No more cherry-picking high-yield pools. The protocol owns the liquidity-and controls it. This isn’t magic. It’s math. Olympus offers bonding: you trade your tokens for OHM at a discount. If you send $1,000 worth of DAI, you might get $1,200 worth of OHM. The protocol uses that OHM to buy LP tokens. Now, it owns the pool. You get OHM. The protocol gets control. And because the protocol holds the liquidity, it doesn’t need to pay you 50% APY to keep you there. Tokemak took this further. It turned liquidity into a service. Protocols pay TOKE tokens to direct where liquidity flows. Tokemak’s 2025 report showed its model reduced market depth volatility by 85% compared to traditional mining. That means less slippage, more stable prices, and better trades for everyone.Why Most LPs Lose Money

The biggest lie in DeFi is that "high APY" means "safe profit." Here’s what actually happens:- Impermanent loss hits hardest with volatile assets. A user on Reddit, u/LP_Warrior, put $50,000 into ETH/USDC in January 2025. He earned 14.2% in rewards. But ETH dropped 22%. His net loss? 28.7% of his principal. Rewards didn’t cover the loss.

- Token rewards crash. In 2025, 17 protocols saw their incentive tokens fall over 60% in value. Your 10% APY in token rewards? Worth 3% after the drop. That’s negative net return.

- Gas fees kill small accounts. On Ethereum, each swap costs $1.20-$3.50. If you’re only putting in $2,000, and you have to claim rewards every 48 hours? You’re paying $100+ in gas per month. That’s 5% of your capital gone before you even earn.

- Unstaking is a nightmare. Trustpilot data shows 62% of negative reviews cite "unpredictable rewards" and "complex unstaking." Some platforms lock funds for 30 days. Others require voting weights. One protocol asked users to hold veCRV for 16 weeks just to get full rewards. That’s not passive income. That’s a part-time job.

What Works in 2026

The winners aren’t chasing the highest APY. They’re playing the long game.- Stablecoin pools win. USDC/USDT on Curve Finance delivered 9.3% net APY over 14 months with near-zero impermanent loss. Why? Because stablecoins don’t swing ±30%. Their value stays flat. The reward comes from fees and CRV emissions-not price swings.

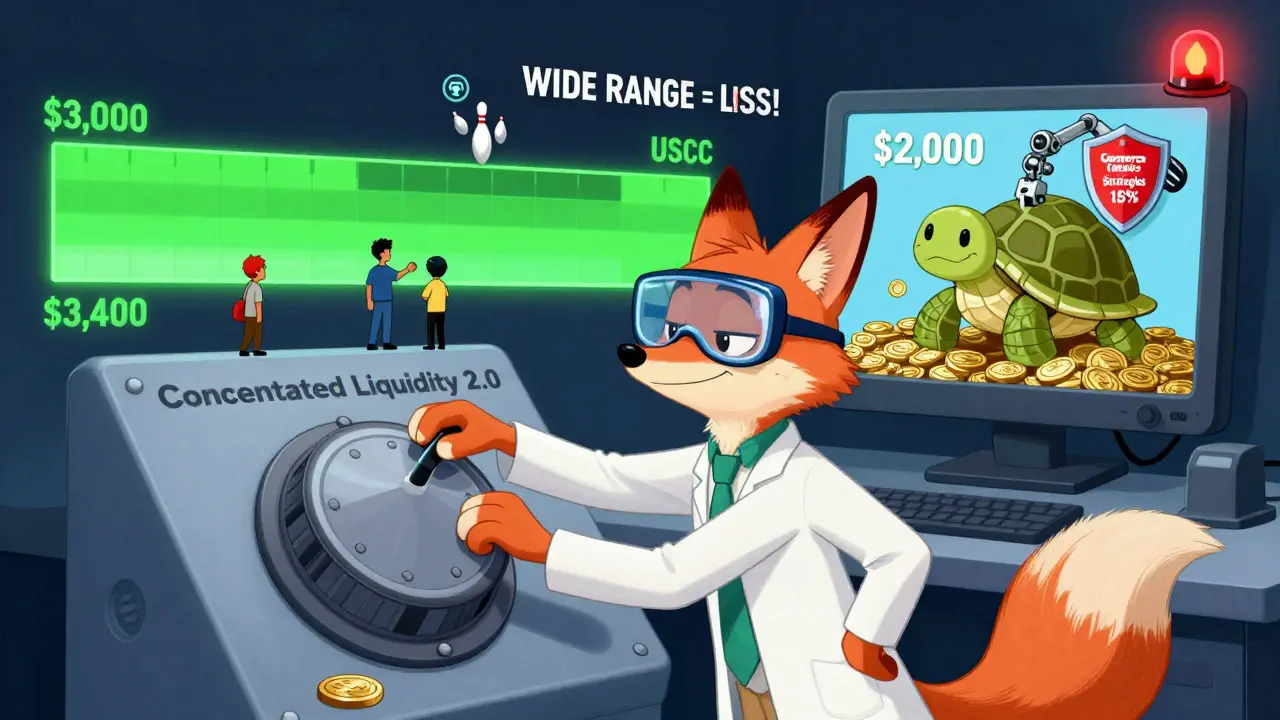

- Concentrated liquidity is key. Uniswap’s 2026 update, "Concentrated Liquidity 2.0," automatically adjusts fee tiers based on volatility. In testing, it cut impermanent loss by 23%. If you’re using Uniswap, you need to set your price range tight. Don’t spread your funds across $1,000 to $5,000. If ETH is at $3,200, set your range from $3,000 to $3,400. That’s where the trades happen.

- Use protection tools. 73% of experienced LPs use tools like Bancor’s IL Protection or Gamma Strategies. These auto-hedge your position. If ETH drops too fast, they sell part of your position to cover losses. They cost a small fee-but they save 15-40% of your capital in crashes.

- Go institutional. Liminal Custody’s Enterprise LP solution now manages $2.4 billion in institutional capital. They don’t rely on token rewards. They use POL models, multi-asset pools, and automated rebalancing. If you have $50,000+, this is the path.

The Future: What’s Changing in 2026

The era of "just stake and earn" is over. Here’s what’s coming:- Ethereum’s Pectra upgrade (Q2 2026) will cut LP staking costs by 40-60%. That means fewer gas headaches, especially for small providers.

- Tokemak’s Reactor 2.0 (Q3 2026) will route liquidity across chains. No more bridging. No more 72-hour waits. Cross-chain LPs will become seamless.

- Curve’s gauges v3 now allocates 40% of CRV emissions to protocol-owned liquidity. That means if you’re not part of POL, you’re getting less reward.

- Regulation is here. The SEC classified some token rewards as securities. 32% of U.S.-accessible DeFi platforms now require KYC. If you’re in the U.S., you can’t just connect your wallet anymore. You need to verify your identity.

Three Rules for Surviving as an LP in 2026

- Never chase APY above 10%. Anything over 10% is either unsustainable or built on a collapsing token. Stick to pools with stable assets and fee yields under 8%.

- Use concentrated liquidity. On Uniswap V3, set your range to ±10% of the current price. Wider ranges = more impermanent loss. Tight ranges = more fees.

- Only use protocols with POL. If a protocol doesn’t own at least 30% of its own liquidity, it’s still renting. That means it’s one bad market day away from a liquidity death spiral.

Protocol incentives aren’t about free money. They’re about aligning incentives. The best protocols don’t bribe you with tokens. They make it profitable to stay. And in 2026, that’s the only way to win.

What is impermanent loss and why does it hurt liquidity providers?

Impermanent loss happens when the price of two assets in a liquidity pool changes after you deposit them. If you put in 50% ETH and 50% USDC, and ETH drops 30%, your share of the pool will be worth less than if you’d just held the tokens. The loss is "impermanent" because if the price goes back, you break even. But in volatile markets, prices rarely return. Most LPs never recover their losses, even if they earn reward tokens.

Is liquidity mining still worth it in 2026?

Only if you’re using stablecoin pairs like USDC/USDT on Curve or similar low-volatility pools. For volatile pairs like ETH/USDC or SOL/USDC, traditional liquidity mining is a losing game. The average LP loses 15-25% of capital annually to impermanent loss, even with rewards. The only sustainable models now are protocol-owned liquidity (POL) and concentrated liquidity with automated hedging.

How do protocol-owned liquidity (POL) models work?

Instead of paying users to supply liquidity, the protocol buys liquidity itself using its treasury. Users can "bond" their tokens (like DAI or ETH) to the protocol in exchange for discounted protocol tokens (like OHM). The protocol then uses those tokens to buy LP positions. This means the protocol owns the liquidity, not users. It reduces churn, eliminates reward volatility, and creates long-term stability. OlympusDAO and Tokemak are the leaders in this model.

What’s the difference between Uniswap V3 and Curve Finance for LPs?

Uniswap V3 is for volatile assets and advanced users. It lets you concentrate liquidity in narrow price ranges, which boosts fees-but increases risk. Curve Finance is for stablecoins. It uses mathematical formulas to minimize price slippage between similar assets (like USDC and USDT). Its rewards are lower, but impermanent loss is near zero. If you want safety, use Curve. If you want higher returns and can manage ranges, use Uniswap V3.

Are there any tools to protect against impermanent loss?

Yes. Tools like Bancor’s IL Protection and Gamma Strategies automatically hedge your position when prices move too far. They sell part of your assets to lock in gains or limit losses. These tools cost a small fee (0.5-1% per trade), but they’ve saved LPs 15-40% of their capital in market crashes. 73% of experienced LPs use them.

Should I use a centralized exchange like Binance instead of DeFi for liquidity?

For most people, yes. Centralized exchanges offer stable, low-fee liquidity programs with no smart contract risk. DeFi rewards are higher-but you’re exposed to hacks, failed contracts, and token crashes. If you’re not actively managing your position, using Binance’s liquidity mining or similar services is safer. DeFi only makes sense if you’re willing to learn advanced tools, monitor prices, and accept the risk.

Next Steps for New LPs

- If you have under $5,000: Start with USDC/USDT on Curve Finance. Use the native wallet. Don’t touch reward tokens. Just collect fees.

- If you have $10,000+: Use Uniswap V3 with concentrated liquidity. Set a tight price range. Enable Gamma Strategies for protection.

- If you have $50,000+: Look into institutional LP solutions like Liminal Custody. They use POL, automated rebalancing, and insurance.

- Always use InsurAce or similar insurance. It costs 0.85% annually-but covers 85% of top protocols.

The game has changed. The old model of "deposit, earn, withdraw" is dead. To survive as a liquidity provider in 2026, you need strategy, tools, and discipline-not just a wallet and a dream.